Understanding Your Credit Score: Why It Matters and How to Improve It

1. Introduction

Your credit score is more than just a number—it’s a key factor that influences many aspects of your financial life. From getting approved for a loan or credit card to securing a good interest rate, your credit score plays a vital role. This article will explain what a credit score is, why it matters, and provide practical steps you can take to improve and maintain a healthy credit profile.

2. What Is a Credit Score?

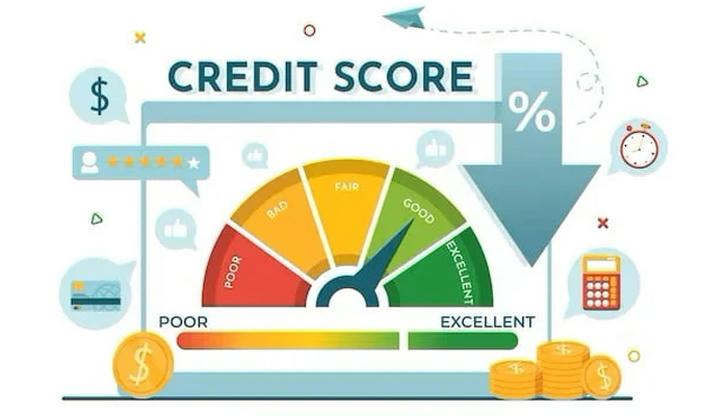

A credit score is a three-digit number that summarizes your creditworthiness based on your credit history. The most commonly used scoring models are FICO and VantageScore, with scores typically ranging from 300 to 850. A higher score indicates better creditworthiness.

- 300–579: Poor

- 580–669: Fair

- 670–739: Good

- 740–799: Very Good

- 800–850: Excellent

Lenders use these scores to estimate how likely you are to repay borrowed money.

3. Why Your Credit Score Matters

Your credit score affects more than just loan approvals:

- Loan and Credit Card Approvals: Higher scores increase your chances of getting approved.

- Interest Rates: Better scores usually mean lower interest rates, saving you money.

- Rental Applications: Landlords often check credit to evaluate tenants.

- Insurance Premiums: Some insurers use credit scores to set rates.

- Employment: Certain employers check credit reports as part of hiring.

A good credit score opens doors to better financial opportunities and saves you money in the long run.

4. Factors That Affect Your Credit Score

Your credit score is calculated based on several factors:

- Payment History (35%): Whether you pay bills on time.

- Credit Utilization (30%): How much credit you use compared to your total available credit. Ideally, keep this below 30%.

- Length of Credit History (15%): Older credit accounts improve your score.

- Credit Mix (10%): Having different types of credit (credit cards, loans) can help.

- New Credit (10%): Frequent credit inquiries or new accounts can lower your score temporarily.

Understanding these can help you manage your credit wisely.

5. How to Check Your Credit Score and Report

Regularly checking your credit helps you monitor your financial health and detect errors or fraud early.

- Free Credit Scores: Many websites and apps offer free access to your credit score.

- Credit Reports: You can get a free credit report annually from each of the three major credit bureaus — Equifax, Experian, and TransUnion — at AnnualCreditReport.com.

- Review Carefully: Check for incorrect information like accounts that don’t belong to you or wrong balances.

6. Practical Steps to Improve Your Credit Score

Improving your credit score takes time and discipline. Here are proven strategies:

- Pay Bills On Time: Timely payments are crucial; even one missed payment can hurt your score.

- Keep Credit Utilization Low: Aim to use less than 30% of your available credit on each card.

- Avoid Opening Many New Accounts Quickly: Multiple credit applications can lower your score.

- Maintain a Healthy Credit Mix: Use different types of credit responsibly.

- Dispute Errors: If you find mistakes on your credit report, report them to the credit bureaus immediately.

- Manage Debt: Pay down existing debt methodically and avoid letting accounts go to collections.

7. Tips for Building Credit from Scratch

If you don’t have a credit history, here’s how to start:

- Secured Credit Cards: Cards backed by a security deposit help build credit.

- Authorized User: Become an authorized user on a trusted family member’s credit card.

- Credit-Builder Loans: Small loans designed to build credit when repaid on time.

- Use Credit Responsibly: Make small purchases and pay them off monthly.

8. Common Pitfalls to Avoid

Avoid these mistakes that can damage your credit:

- Missing payments or paying late.

- Maxing out credit cards or using too much credit.

- Closing old credit accounts unnecessarily, which can shorten your credit history.

- Applying for multiple loans or credit cards in a short time.

9. When to Seek Professional Help

If your credit issues feel overwhelming:

- Consider credit counseling services for guidance on managing debt.

- Debt management programs can help consolidate and pay down debt.

- Beware of credit repair scams promising quick fixes; legitimate improvement takes time and effort.

10. Conclusion

Your credit score matters because it influences many financial decisions and opportunities. By understanding how credit scores work and following practical steps—paying on time, keeping balances low, and monitoring your credit—you can improve your credit health. Healthy credit habits not only save you money but also open doors to a more secure financial future.